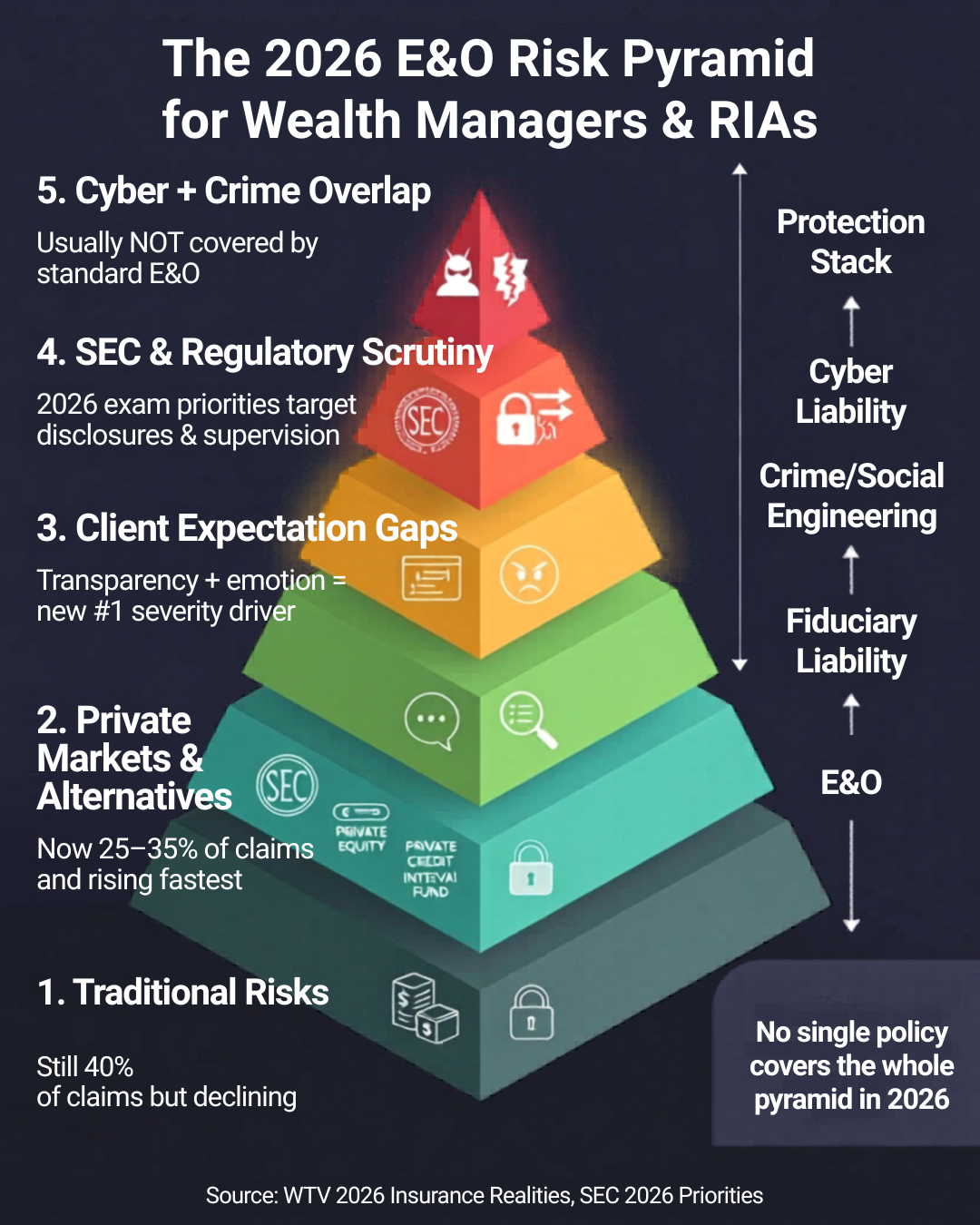

Key Takeaways (TL;DR)

- E&O insurance for RIAs is a critical safeguard for wealth managers in 2026 as client expectations rise, regulatory scrutiny intensifies and portfolio complexity increases. Claims are often driven by suitability disputes, disclosure gaps and operational errors rather than misconduct.

- Private-market investments are contributing to higher claim frequency across the industry due to valuation ambiguity, liquidity constraints and disclosure challenges. However, coverage availability depends on whether those investments fall within the scope of an advisor’s E&O policy and certain strategies may be excluded.

- Strong documentation, consistent supervision and clear communication remain the most effective ways to reduce claim exposure and support favorable outcomes when disputes arise.

The Rising Risk Environment Wealth Managers Face

Wealth managers operate in a more demanding and complex environment than ever before. Clients expect real-time visibility, personalized strategies and proactive guidance across investment, tax and planning decisions, especially during periods of volatility. At the same time, portfolios increasingly include alternative strategies, structured products and other investments that are harder to explain and monitor.

This combination increases the likelihood of disputes. When outcomes differ from expectations, clients are more likely to question whether advice, communication or execution met their expectations. For high-net-worth clients, even small misunderstandings can escalate into formal claims.

This article explains why expanding client expectations and growing portfolio complexity are key drivers behind rising E&O exposure across the wealth management industry, and why errors and omissions insurance coverage has become an essential safeguard in a modern wealth manager’s business model.

Caption: Source: Based on 2025-2026 trends from WTW & SEC priorities. Coverage varies by policy.

Private Markets as a Primary Driver of E&O Risk

Private-market investments are now a common component of sophisticated portfolios, but they introduce risks that are structurally different from traditional assets. These investments often involve limited liquidity, less transparent pricing and more complex disclosures, all of which increase the potential for misunderstandings and client disputes.

Disputes frequently arise when:

- valuations change unexpectedly

- redemption restrictions limit access to capital

- performance behaves differently than anticipated

Clients may believe they understand these risks at the time of investment, but expectations often shift when market conditions change or liquidity is needed. High-net-worth (HNW) clients are often legally sophisticated and more likely to pursue claims when disputes arise. Even minor administrative missteps or communication gaps can become the foundation for litigation if a client believes their advisor failed to meet a professional obligation.

While private-market activity is contributing to higher claim frequency across the industry, coverage availability depends on whether the underlying investments fall within the scope of the advisor’s E&O policy, notably when certain strategies may be excluded.

Industry data reinforces this shift. iCapital reports that RIA adoption of private-market investments has grown from roughly one-third of firms in 2022 to a projected majority, while valuation opacity is contributing to a meaningful share of client disputes. At the same time, SEC exam priorities for 2026 continue to emphasize disclosures and oversight tied to these strategies.

Taken together, these trends help explain why claim frequency and severity are increasing across the industry, not that E&O coverage universally applies to private-market activity.

What E&O Insurance Covers and Where It Might Not Apply

E&O insurance for investment advisors protects wealth managers against claims alleging negligence, misrepresentation or errors in professional services. Most claims stem from disagreements about advice, communication or execution rather than intentional wrongdoing.

Core protections within a strong E&O policy

A well-structured E&O policy generally responds to claims involving:

- suitability and allocation decisions

- inaccurate or incomplete disclosures

- communication gaps or misunderstandings

- administrative or operational errors

- failure to follow client instructions

- supervisory breakdowns within a firm

These scenarios often hinge on documentation. When records clearly support the advisor’s process and communication, the firm is better positioned to defend against claims.

Common E&O exclusions and limitations

E&O insurance is not designed to cover every type of loss. It generally does not apply to:

- losses tied to investments outside the advisor’s approved or eligible scope, including private equity investments and private placements.

- intentional misconduct or fraud

- regulatory fines or penalties

- custodial or third-party failures

- cyber incidents unless specifically endorsed

This is particularly important in the context of private markets. Even when a dispute involves alleged misrepresentation, coverage depends on whether the investment itself is eligible under the policy.

Because of those boundaries and that E&O policies focus on unintentional errors, any scenario involving intentional misconduct, fraudulent behavior or regulatory fines sits outside the policy’s protection zone. This is why E&O typically works alongside other coverages, including cyber liability insurance and fidelity bonds.

Where E&O Claims Actually Occur in Practice

Most E&O claims fall into a few consistent categories that reflect how advisory relationships function in real-world conditions. These disputes often involve mismatched expectations and can lead to substantial E&O exposure. KKR projects RIA private exposure rising from 43% minimal allocations in 2025 to 91% significant by 2027.

Suitability and allocation disputes

Suitability remains the most common source of claims. Clients may reassess their risk tolerance after market volatility and argue that a portfolio was too aggressive or not aligned with their objectives. These disputes often depend on whether the advisor can demonstrate a clear suitability process supported by documentation.

In these cases, the advisor’s documentation is critical to keep on file, including investment policy statements, meeting notes and risk assessments. Without a clear record, clients may argue that the allocation was inappropriate given their needs.

Disclosure and communication gaps

Claims frequently arise when clients believe risks were not fully explained. This may involve liquidity constraints, fees, tax treatment or the structure of complex products. Even when disclosures were provided, disputes can occur if documentation does not clearly show that the client understood them. If the advisor believes a client understood the liquidity constraints of a private-market investment, but the client later alleges they were misled, the dispute may hinge entirely on documentation quality.

Operational and supervisory breakdowns

Administrative errors and inconsistent supervision also contribute significantly to claims. Missed instructions, delayed transactions or documentation inconsistencies can lead to financial harm or client dissatisfaction. As firms grow, gaps in oversight and communication between team members can increase exposure.

Private-market investments often amplify these risks because they combine complexity, limited transparency and heightened client expectations.

Regulatory and Compliance Pressures Increasing Exposure

Regulatory scrutiny continues to intensify, particularly around disclosures, fees and conflicts of interest. SEC examinations now require more detailed documentation and a clearer demonstration of how advisors make and supervise decisions.

Areas of focus commonly include:

- accuracy of fee disclosures

- consistency of investment processes

- documentation of client communication

- oversight of complex or alternative investments

- identification and management of conflicts

Cybersecurity has also become part of the broader supervisory landscape. While most cyber incidents fall under cyber liability coverage, regulators increasingly view cybersecurity preparedness as a component of firm oversight. If a cyber event leads to client losses or operational disruption, it may trigger E&O claims tied to supervision or disclosure failures.

This environment reinforces the importance of aligning documentation, communication and supervisory practices with regulatory expectations.

How NAPA Premier Supports Advisors Facing Rising Liability Risk

NAPA Premier supports wealth managers by aligning coverage structure with the way advisory firms operate. This includes reviewing the firm’s client profile, investment approach and supervisory structure so coverage terms and exclusions are clearly understood before a claim occurs.

A typical review focuses on how suitability and risk discussions are documented; how supervisory workflows are structured; how investment strategies are described and communicated; and how underwriting expectations apply to the firm’s model.

NAPA Premier also helps clarify how E&O, cyber liability and fidelity bonds work together so advisors understand where each policy responds and where gaps may exist.

90-Day Checklist for Wealth Managers

Over the next 90 days, wealth managers can strengthen their risk posture by focusing on a few key areas:

- Review E&O limits, exclusions and endorsements to ensure they match exposure

- Evaluate documentation processes for suitability and disclosures

- Reassess exposure to alternative and complex investments

- Strengthen supervisory and review workflows

- Improve consistency of client communication records

These steps help reduce exposure while positioning the firm for a more effective underwriting review.

The Bottom Line

Wealth managers face increasing liability as client expectations rise, portfolios become more complex and regulatory oversight expands. E&O insurance remains a foundational safeguard for eligible advisory activities, but its effectiveness depends on understanding where coverage applies and where limitations exist.

Firms that prioritize documentation, maintain consistent supervision and clarify expectations with clients are better positioned to manage disputes and protect long-term stability.

This is especially important as private-market investments become more prevalent, since many E&O policies, including programs such as NAPA Premier, may exclude certain strategies or limit coverage based on investment eligibility.

FAQs

What are the most common E&O claims for wealth managers?

Most claims involve suitability disputes, disclosure gaps and operational errors. These typically arise from misalignment between client expectations and documented advice or communication.

How do private-market investments increase E&O risk?

Private market investments introduce valuation uncertainty, limited liquidity and complex disclosures, which can lead to misunderstandings. Most E&O policies, NAPA Premier included, have exclusions on private market investments, so check whether those investments and certain strategies are eligible under the E&O policy.

What does E&O insurance typically cover for advisors?

E&O generally covers claims related to professional services such as investment advice, communication errors and administrative mistakes. Coverage depends on policy terms and the eligibility of the underlying activity.

How much E&O coverage should a wealth manager carry?

Coverage needs vary based on client profile, assets under management and investment complexity. Most E&O policies for RIAs often start around $1,000,000 per claim and $1,000,000 annual aggregate, but those limits may be insufficient for firms with higher exposure. Wealth managers serving high-net-worth clients, managing larger AUM or incorporating more complex or alternative strategies often consider higher limits to better align with potential claim severity and defense costs.

Schedule your free consultation with an insurance expert today to discuss your coverage needs, custodian requirements, pricing and next steps.